Understanding the UK's Audio-Visual Expenditure Credit (AVEC), Video Games Expenditure Credit (VGEC), and how these relief changes will impact production budgets.

On July 18, 2023 the UK government published draft legislation on the reform of the UK creative sector tax reliefs. The reform was announced by Chancellor Jeremy Hunt in the March 2023 Budget following a period of consultation at the end of 2022.

Thankfully, the draft legislation largely mirrors what was set out in the Chancellor’s original proposal. Now that we have a little more certainty about the future of the tax reliefs, let’s examine some of the key changes.

What is the new relief?

The new relief, the Audio-Visual Expenditure Credit (AVEC), combines four of the existing cultural sector tax reliefs:

- Film;

- High-end TV (HETV);

- Children's TV; and

- Animation

A new Video Games Expenditure Credit (VGEC) will also be introduced at the same time, replacing the current video games tax credit.

The operation of the relief is slightly different in that, rather than it being considered a tax refund from HMRC, the AVEC and VGEC will be payable expenditure credits that will then be taxed (in a similar way to a grant) on normal corporation tax rules (see below).

How much is the new relief worth?

When first announced, there was some initial excitement that the rate of credit had increased from 25% to 34% – which was indeed the headline rate referenced by the Chancellor. However, as mentioned above, the AVEC is now taxable; therefore, when the notional rate of corporation tax (25%) is applied, the actual payable amount under the new system will be 25.5% (being 75% of 34%).

There has been a significant increase for both animation and children’s TV, with the expenditure credit rate for those streams now set to 39%, giving an effective payable rate of 29.25% – a great show of support for these sectors.

Will I have to plan my cash flow to pay a tax bill now?

The short answer is no.

The tax payable on the AVEC/VGEC will form part of the overall tax computation for the period in question, alongside the calculation of the credit to be received. As such, it forms an almost notional tax charge from a calculation perspective and HMRC will settle the “net” amount to the production company.

From a cash flow perspective, there should therefore be no real difference compared with the current system.

Notably, there is already precedent for this in the UK. The current Research and Development Expenditure Credit (RDEC) is administered in the same way; therefore, the HMRC infrastructure is in place and well tested to handle this system, so the transition should be smooth.

What if the UK corporation tax rate changes?

This is a logical question to consider. As the expenditure credit is now taxable, if the corporation tax rate changes, the value of the credit could rise or fall in line with this.

For instance, the previous rate of 19% would have set the new value of the credit at 27.5% – a notable increase in value.

Based on the initial draft legislation, the rates of relief have been fixed at 34% and 39% as set out above without reference to the main rate of corporation tax opening the potential for a variable rate of relief which would clearly cause uncertainty for productions. Enquiries have been made of HMRC as to their intent in this regard and how it may work in the future should the rate of corporation tax change.

Does this change what I can claim on?

There is more good news on this front; so far, there have been no changes to what can be claimed on. At present, the underlying operation of what is qualifying spend and what is not has changed and therefore the collective precedent that has been built up with HMRC for allowable claims remains in place.

One thing that is worth noting is that in its response to the consultation, the government has introduced an anti-abuse measure on payments between connected parties to restrict qualifying expenditure to the costs incurred by the group.

The anti-avoidance measures introduced by the new legislation revolve mostly around disallowing from tax credit (but importantly not from budget) items or elements of items that represent “connected party profit.” In practice, this means that if Company 1 pays connected Company 2 £100 for a service, and providing that service costs Company 2 only £75, Company 1’s qualifying expenditure will be limited to £75 for tax relief purposes. This applies across an entire group irrespective of whether there are three, four or more companies in the “chain” leading to the claimant company.

An important exclusion from this is that expenditure relating to leasing, hiring or accessing locations or buildings for principal photography will not be restricted. Therefore, intra-group costs for studio space do not follow the above restriction – provided of course that the costs charged are at an arm’s length rate as required for all intra-group transactions.

For HETV productions, there has long been the concept of the “Production Fee” charged in the budget by the owner of the SPV making the show for the broadcaster. Historically, this has been an eligible production cost but under the new anti-avoidance measures, there is a question as to whether this could fall foul of the new connected party profit rules.

As with the corporation tax rates above, clarity from HMRC has been requested. Keep an eye on the EP Blog for updates.

I heard the HETV minimum spend will increase from £1m per hour, is that correct?

Interestingly, the £1m per hour threshold was not one of the elements where the government requested specific responses, although the initial consultation noted that such a move was being considered. This prompted most respondents to use the ‘open response’ section to provide views on this and – to quote the government’s response to the consultation – “responses to the suggestion of raising the threshold were overwhelmingly negative.”

The threshold has therefore been retained at £1m per hour, although the government has stated that it will continue to review this.

How about the cultural test?

As with the qualifying expenditure and HETV £1m per hour thresholds, there has been no change to the cultural test following the consultation. Films and programmes will still have to pass the relevant cultural test to qualify for AVEC/VGEC exactly as before.

What difference will I actually notice?

This is a reasonable question given that the message so far has been no changes other than a 0.5% uplift for Film and HETV and a 4.25% uplift for children’s TV and animation.

Outside the above, the first key change to note is that the slot length for qualification of an HETV programme has moved from 30 minutes to 20 minutes. This is to create consistency between streaming and linear TV requirements for programmes that would be 30 minutes on linear but only approximately 23 minutes on a streaming platform.

The government has also clarified that this is to be applied on an episode-by-episode basis and should not be looked at across the combined length of the commissioned programme. While this was the general interpretation in any case, there were some applications on the latter basis which was not the original intention, and it should prevent ‘boundary pushing’ applications where very small videos were grouped together to meet the 30-minute requirement (again not the intention of the original legislation).

The second (and most visible) difference is the presentation of the credit within the financial statements. Rather than showing as taxable income, the AVEC will reduce the costs and the tax charge on it will show as a taxable expense.

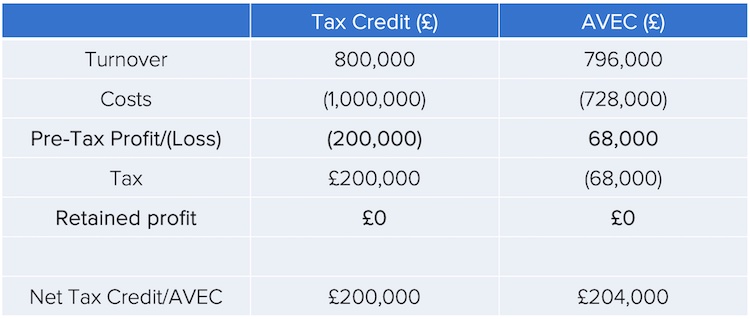

Let’s take as an example a film with costs of £1m, where all are UK used and consumed and eligible for the tax credit. Under the ‘old’ system, the film would qualify for a tax credit of £200,000 (25% of 80% of expenses).

Under AVEC, the credit would be £272,000 (34% of 80%), giving net expenses of £728,000. Only the AVEC would be taxable (there being a loss pre-AVEC of £200,000), creating a tax bill at 25% of £68,000.

You will note that turnover is different between the two examples. This is because most agreements would define the purchase price of a film as the cost of the show net of incentives; therefore, the £4,000 additional credit under AVEC would reduce the turnover by £4,000 as well.

What are the next steps and timeline for the changes?

The government is due to enact the legislation in the autumn, which would make the new AVEC/VGEC available from January 1, 2024.

Productions that straddle January 1, 2024 may elect to transition to the new regime from that date and attract the 25.5% rate of relief rather than the existing 25% rate.

Any production that has not commenced principal photography by April 1, 2025 will only be able to use the new AVEC scheme. However, productions which are ongoing as at April 1, 2025 may continue to use the old regime if they wish up to the ultimate sunset date.

The ultimate sunset for the current regime is March 31, 2027 – quite some time away – which has been set to ensure that longer running productions, such as animations, are not impacted mid-production. From April 1, 2027, the only available regime will be AVEC/VGEC.

Due to their nature, the changes will mostly impact advisers, accountants, and lawyers, rather than directly impacting producers and the creative side, other than budgeting for the small uplift. It’s therefore important to make sure that you engage advisers who are confident with the new legislation and regime.

How Entertainment Partners can help

As the UK incentives landscape continues to evolve, the Entertainment Partners team wants to make sure you understand how it impacts your productions. Keep an eye on our site for updates and if you ever have questions or need support, please contact us.

If you decide to explore the UK as a filming destination, reach out to Lloyd Gunton and the team at FLB Accountants (an Entertainment Partners company). FLB is a UK-based chartered accounting firm with expertise in media and entertainment accounting, tax and tax incentives, finance, and accounting. They also provide film and TV tax credit incentive estimates and formal opinions to lenders, manage tax credit claim submissions, work with producers to advise on, finalise budgets, and provide deal close support for both independent and multi-party financed projects.

And when you’re ready to start shooting, EP has the digital solutions you need to manage your UK productions from prep to wrap, including digital onboarding, timesheets and payroll. If you’d like to learn more about how we can support you, please get in touch.

Neither Entertainment Partners nor FLB Accountants are providing legal, tax or financial advice in this article to be relied upon. This article is for information purposes only. Please do take advice on this area where your specific circumstances can be considered.

Never miss an article by our experts! Check out our entire library of blogs at ep.com/blog.