What production workers need to know when being hired on productions through a loan-out company in Canada.

Canada’s vibrant film and television production industry creates over 200,000 jobs each year. While many crew and cast members are hired by productions as employees or self-employed individuals, others are hired through a corporation—commonly referred to as a ‘loan-out’ company. In this post, we’ll define what a loan-out is, and what to keep in mind if choosing to work through a loan-out on productions, including some of the tax and compliance responsibilities that impact loan-out owners.

Loan-out basics

A loan out-company is most commonly a single-owner company where an individual selling their talent or services owns the company, serves as the officer and director of their company, and may be its sole employee. Loan-outs are set up as a separate legal entity and are hired via contract signed by both the production and the loan out, as the business entity the worker is being hired through.

Productions can claim tax credits for payments made to workers being paid through their loan-out company. However, productions can lose their tax credits if a loan-out company isn’t in compliance.

For this reason, being hired as a loan-out means the production is taking on risk and choosing whether to employ individuals through a corporation is fully at their discretion. In other words, it’s within the production’s right to decline a person’s request to be paid through their loan-out and pay them as an individual instead.

Keeping a loan-out in compliance

As separate legal entities, loan-outs are required to make annual compliance filings. If you miss a series of annual filings, your company may be dissolved for non-compliance and you’ll need to apply to have it revived, which can really cost you down the road.

You will also need to keep your corporate records up to date. Sometimes described as “minute book documents” these documents record details about your loan out, including its officers, directors and shareholders.

One of these documents is your Shareholder Register or Central Securities Register. This document provides a list of corporate shareholders and shows 1) how many shares each one owns, 2) at what value, and 3) when they were issued. This is one of the documents a production may need from you to confirm your loan-out’s ownership status for tax credit purposes.While there may be advantages to setting up and employing a loan-out, there are several other considerations to keep in mind which are beyond the scope of this article.

Briefly, some of the pitfalls and issues to consider with loan-outs are:

- Assessing whether CRA would consider the loan-out a “personal services business” and how that can impact its tax situation;

- GST/HST collection and filing requirements;

- Whether the loan out requires workers compensation coverage based on the rules in the province in which it operates;

- Obligations of the shareholder or operator of the loan-out to ensure all payroll requirements are met, where applicable.

If you decide to set up a loan-out, it’s important to make sure all steps are completed correctly, and nothing is missed. Although you can incorporate a loan-out on your own, enlisting the services of a law firm and CPA firm will help ensure all compliance obligations are met.

Corporate tax filings: Understanding how the fiscal year applies to loan-outs

Much like individuals who must file a T1 income tax return each year, loan-out corporations also have annual tax filing requirements. However, unlike individuals, loan-out owners can choose the start and end date of their company’s fiscal year. Once set, the corporation is required to file a T2 corporate income tax return for the 12-month period leading up to and ending on the corporation’s year-end date—known as the ‘fiscal year-end’—on an annual basis.

For example, if a company chooses March 31 as its year-end, its fiscal period runs from April 1 to March 31 of the following year for all future filings, and that 12-month period will be covered on the corporation’s tax return each year.

Corporations must file a T2 income tax return within six months of the corporation’s year-end date. Canada Revenue Agency (CRA) then issues a Notice of Assessment (NOA)—which serves as a ‘receipt’ for your loan-out’s tax return. Once filed, it typically takes CRA two to four months to issue an NOA.

Proving tax compliance to a production for tax credit purposes

When a production engages a loan-out corporation, the loan-out is required to prove it has complied with its tax filing obligations. The type of proof depends on a number of factors.

Timeline for existing corporations

Existing loan-out corporations must prove tax compliance by providing two things:

- The NOA that was issued for its most recent T2 corporate tax return, and

- The Schedule 50 that was filed with its most recent T2 corporate tax return

All existing corporations should be able to provide both of these documents, if they are up-to-date and compliant with their tax filing requirements.

A production’s request for the “most recent” tax return refers to documents from the tax return that the corporation should have available, at the present time. Again, this will vary by corporation, at different times in the year, due to companies having different fiscal year ends.

For example, if a production requests documents for your “2024 or current year-end”, you’d send documents that cover the 12-month period preceding the company’s year-end date that occurred in the 2024 calendar year. This can be confusing because the beginning of this 12-month period could have started in 2023 but will have ended in 2024 (e.g. the most recent 12-month period for a loan-out with a March 31 year end would have run from April 1, 2023 to March 31, 2024). If your current year’s tax filing isn’t yet due or you haven’t yet received your 2024 NOA, then you would provide the production with your most recently filed – i.e. 2023 NOA and Schedule 50 – documents.

If you’re able to provide an NOA and Schedule 50 for a tax year-end that falls within the acceptable date range, that’s a wrap! You proved compliance to the production.

Timeline for newly formed corporations

If you are newly incorporated and there is a delay in receiving your NOA, it’s not time to panic yet. Productions frequently provide a two-month cushion, which allows corporations to provide documentation from the prior fiscal year for up to 24 months.

Newly formed companies that were incorporated less than 18 months before being hired on a production can provide:

- Articles of Incorporation: used to show that the company is up to 18 months old, and

- Shareholder or Central Securities Register: always available, since it was created during incorporation.

Between 18 and 24 months, loan-outs that have filed a tax return but don’t yet have a corporate NOA can provide:

- Articles of Incorporation: used to show that the company is up to 24 months old, and

- Schedule 50 (that was filed with its T2 return) if available, or if not, its Shareholder Register (always available), and

- NOA issued for the owner’s personal T1 income tax return.

Beyond 24 months from your loan-out’s formation, as noted above, your company’s most recent NOA and Schedule 50 will be required to prove compliance.

Submitting the right paperwork

Finally, there are a few helpful tips corporations should be aware of to ensure that they are providing all of the required information to productions, when submitting compliance documents.

Corporations should always provide page 2 of their NOA, as this shows the date of the tax year-end being assessed.

The first page of the corporate Notice of Assessment only shows the date that the assessment was issued, it does not indicate the tax year-end that assessment is being issued for. If a corporation only provides page 1 of the assessment, the production will not have the information it requires.

Page 1 – not sufficient:

Page 2 – required:

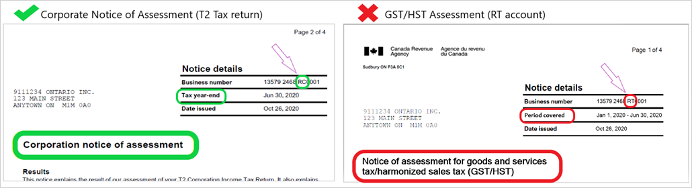

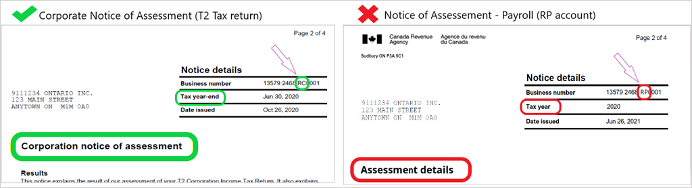

Note that CRA issues various “assessments” to corporations that all look fairly similar, such as sales tax assessments, payroll remittance assessments, etc.

No other assessments besides the NOA are acceptable documents, for tax credit purposes.

The document that productions require is the assessment for the corporation’s income tax filing. You can identify this assessment because it will be issued to your corporation’s “RC” account. And it will be issued for a “tax year-end” date.

Other assessments will be issued to another account (“RT”, “RP”, etc.) and will be issued for a different date or date range, such as “period covered” or “tax year”.

Here are some examples that show how to identify these documents:

Operating a loan-out in Canada? Here’s how EP can help.

When it comes to providing the right paperwork to productions, loan-outs have a lot they need to keep track of, but EP is here to help. We created EP Residency - a secure, online solution to collect and manage records of Canadian residency for employees, individuals, and corporate loan-out service providers in Canada. When using EP Residency to submit documents to productions, the system guides you by showing the documents needed and alerting if anything is unacceptable.

Ditch the paper and save the hassle of providing physical copies of the same documentation for each show you work on— documents uploaded to EP Residency are reviewed by EP’s tax credit team, and once a document is approved, it can be used as backup for all future shows, for as long as the document remains valid.

For questions about the suitability of a specific document for tax credit purposes, or to learn more about EP Residency, production workers and production accounting teams can always reach out EP’s Production Incentives team for help.

This article contains general information we are providing on a subject that may be of interest to you. Nothing in this article should be considered legal or tax advice. You should consult with your tax or legal advisors regarding the applicability of any of this information to your specific circumstances.