As the UK government strengthens its support for productions, find out what the latest changes to the incentives regime mean for you.

In the latest budget announced on March 6, 2024, Chancellor Jeremy Hunt included a range of new measures to be introduced to the UK incentive landscape. Combined with the introduction of the Audio-Visual Expenditure Credit (AVEC) earlier this year, this represents the biggest change to the UK incentive landscape in nearly a decade.

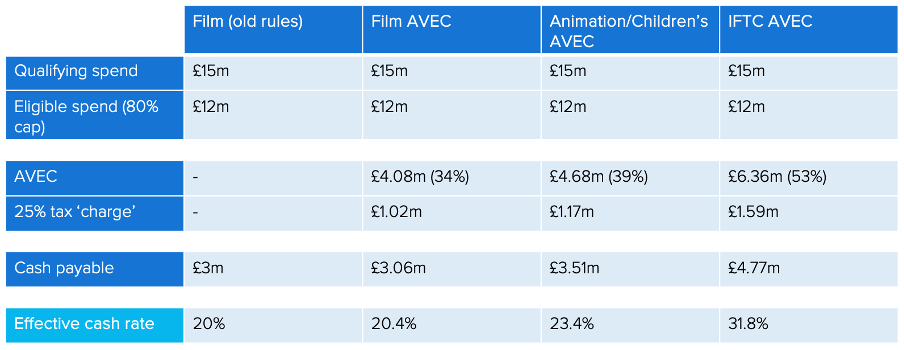

These changes and enhancements underpin the government’s ongoing commitment to the creative sector incentives as they have, in each case, increased the incentive proceeds available on a like-for-like basis (as shown in the table below).

The two main changes from the budget are:

- The introduction of an entirely new Independent Film Tax Credit (IFTC); and

- An enhancement of the rate of credit payable on visual effects (VFX) costs.

While further information is required on a number of key areas, this article sets out what we know so far about how these changes will affect your upcoming productions.

What is the IFTC?

The IFTC is a new credit that sits within the recently introduced AVEC alongside the Film, High-End TV, Animation and Children’s TV regimes. It is an addition to the suite of incentives already available and does not replace any existing incentives.

The relief is aimed at independent film productions with a budget (excluding marketing and distribution costs) of less than £15m.

A new test will also be introduced, to be administered by the British Film Institute (BFI), under which films will need to either:

- Have a UK writer; or

- Have a UK director; or

- Be certified as an official UK co-production

What is the IFTC worth?

The IFTC will have an initial credit rate of 53% of qualifying expenditure. However, as with the AVEC, this rate is subject to UK main rate corporation tax of 25%; therefore, the effective rate of credit is 39.75%.

For comparison purposes, the main AVEC Film effective rate is 25.5%. As such, this new regime represents a staggering 56% increase in the cash value of the incentive that is available to productions.

The existing cap of 80% of total qualifying expenditure will apply to the IFTC (as it does to other AVEC regimes). Therefore, for a production with greater than 80% UK qualifying spend, the effective rate becomes 31.8% (80% x 39.75%).

The following table compares the regimes, assuming a 100% UK production.

What happens if we go over budget?

This is the obvious question that arises with any budget-capped credit – will you be ‘punished’ if the budget overruns and you exceed the £15m level?

Based on the information currently available from HMRC, there is no intent to pull films out of the IFTC regime if they legitimately run over budget and exceed £15m total spend. However, the amount payable under the regime for a given production will be capped at £4.77m (as shown in the table above). Therefore, no additional credit will be generated from the overruns.

The BFI will also be assessing the budgets of films applying for certification under the IFTC to ensure that they can reasonably meet the budget condition. A film that is budgeted to cost close to the £15m limit with no contingency in place should therefore expect some pushback on its ability to meet the condition.

Does this change turnaround times for payment?

Payment times for the IFTC should be the same as they are for the existing Film Tax Relief and the new AVEC – approximately eight weeks from submission to HMRC.

This comes back to the IFTC being an addition to the existing regimes which is calculated in the same manner and subject to the same underlying rules. It just has a different % rate to be applied and a budget cap.

How long will we have to wait to access the new regime?

The new IFTC has a swift implementation and is available to any production where principal photography begins on or after April 1, 2024, where the required criteria are met.

However, claims can only be submitted from April 1, 2025. Therefore, while a project may be eligible for the enhanced rate, there is likely to be a time element to consider in terms of whether it is the right regime to apply for if the credit cannot reasonably be expected to be paid out before late May 2025 at the earliest.

What about the Cultural Test and other ‘standard requirements’ for UK productions?

The standard requirements of any UK production (e.g., film, TV, animation or video game) will still apply to the IFTC.

Therefore, a film must:

- Pass the Cultural Test and be certified culturally British by the BFI;

- Be made by a UK Film Production Company; and

- Incur at least 10% of the production budget on UK ‘used or consumed’ goods

What are the unknowns?

More information is needed on the BFI’s new test to determine whether a film qualifies for the IFTC. Until we have details on this, all we have to go on are the three criteria quoted above, as set out by HMRC.

The other key element that requires clarification is what constitutes an ‘independent’ film. Keep an eye on the EP blog for updates in this space.

This second element is likely going to dictate structuring and rights arrangements for productions, so be sure to seek advice in this respect if you are looking to access the IFTC.

Is the VFX enhancement another new regime?

No – unlike the IFTC, the change to the VFX enhancement is not a new regime but rather a change to the way that the AVEC is calculated on qualifying VFX spend for already qualifying film and HETV productions.

Importantly, you cannot get this enhanced VFX rate for children’s TV or animation productions and HMRC has already explicitly stated that IFTC qualifying productions will not get enhanced VFX credit rates beyond the 39.75% rate.

So, what is the impact of the enhancement?

Qualifying VFX spend will get an additional 5% credit rate, bringing it up to a net rate of 29.25% (34%+5% taxed at 25%). This is the same as the enhanced rates for animation and children’s TV productions, which is why those regimes are also not eligible for the enhancement.

The other element that has changed is that the 80% qualifying spend cap will not apply to UK VFX costs. This means that all UK VFX will be eligible for the incentive irrespective of the overall proportion of the production that is used or consumed in the UK.

What VFX costs qualify for the enhanced relief?

HMRC has already acknowledged to stakeholders that a consultation will be held to determine what type of costs will be in scope for the additional relief. It can reasonably be expected that VFX contract costs will be in scope, but how wide that definition becomes and whether it extends to costs such as on-set VFX data capture personnel remains to be seen.

The best precedent for what might be included is the BFI definition of what qualifies for the purpose of Section C1 of the Cultural Test, which can be found in the BFI guidance notes.

In practicality, how will the exclusion from the 80% cap work?

HMRC has yet to confirm this, but it has stated that it will provide practical guidance on how the relief will work in practice in the coming weeks.

The key will be whether VFX costs are included in the initial calculation of proportion of UK activity and then how the enhanced rate will be incorporated into the overall calculation.

Again, we will provide further information on this as soon as we have it.

Will the VFX rate come into effect at the same time as the IFTC?

Unfortunately not – the VFX changes will not come into effect until April 1, 2025.

This is because unlike the IFTC, which follows the existing regime process, further work is required to agree the definitions and practicalities of the implantation of the VFX enhancement.

Want to know more about these changes?

Please don’t hesitate to get in touch with the team at FLB Accountants (an Entertainment Partners company).

As a UK-based accounting firm with expertise in media and entertainment accounting, tax and tax incentives, finance, and accounting, the FLB team can also provide film and TV tax credit incentive estimates and formal opinions to lenders, manage tax credit claim submissions, work with producers to advise on and finalise budgets and provide deal close support for both independent and multi-party financed projects.

Never miss an article by our experts! Check out our entire library of blogs at ep.com/blog